Examples of Statutory Employees and Their Tax Obligations

When it comes to taxes, how a worker is classified can make a big difference—for both the individual and the business that hires them. While most people are familiar with traditional employees or independent contractors, there's another important classification that’s often misunderstood: the statutory employee. You might be wondering, what is a statutory employee?

This unique status blends elements of both employment and self-employment, creating a distinct set of rules to withhold taxes. Join our Raleigh CPAs answer common questions like 1. What is a statutory employee? 2. How are statutory employees taxed?, 3. What are the tax implications for statutory employees, and more to help you understand this distinct classification.

Table of Contents

What Is a Statutory Employee?

Let's dive right in. What is a statutory employee? A statutory employee is a unique category of worker who falls somewhere between a traditional employee and an independent contractor. While they are technically self-employed, the Internal Revenue Service requires the business they work for to withhold Social Security and Medicare taxes—just like they would for a regular employee. However, statutory employees are still allowed to deduct work related expenses on their personal tax return, which is not typically permitted for standard employees.

Tax Responsibilities for Statutory Employees

Now that you know what a statutory employee is, you might be curious about their tax obligations. Statutory employees occupy a middle ground between being an employee and a self-employed individual. As such, their tax treatment reflects this hybrid status.

W-2 Reporting with Limited Withholding

Although statutory employees are not considered common law employees, they still receive a W-2 form from the business they work with. However, when someone has statutory employee status, their Social Security and Medicare taxes are withheld from their paycheck. Unlike traditional employees, companies do not automatically withhold income taxes, unless the worker specifically requests it.

No Withholding for Federal Income Tax

Because businesses are not required to withhold federal income tax from statutory employees’ pay, the worker is responsible for managing their own estimated tax payments throughout the year. Failing to do so can result in underpayment penalties, so staying on top of quarterly tax payments is essential.

Use of Schedule C for Expense Deductions

Statutory employees can deduct work related expenses by filing a Schedule C (Profit or Loss from Business) with their personal income tax return. This is a major distinction from common law employees, whose tax deductions cannot be unreimbursed for job expenses under current tax law.

Partial Employment Tax Responsibility

While the business pays half of the statutory employee's FICA taxes (just like with traditional employees), statutory employees are still considered self-employed in some respects. They are not subject to unemployment tax, and they may be responsible for certain other obligations if they run additional independent business activity.

Examples of Statutory Employees

To be classified as statutory employees eligible to deduct business expenses, a worker must fall into specific job categories defined by the IRS. These roles typically involve a mix of employer control and independent work, which is why they receive special tax treatment.

Here are some of the most common examples.

How Statutory Employees Differ from Other Worker Types

While statutory employees share certain characteristics with both traditional employees and independent contractors, their tax treatment and work arrangements set them apart.

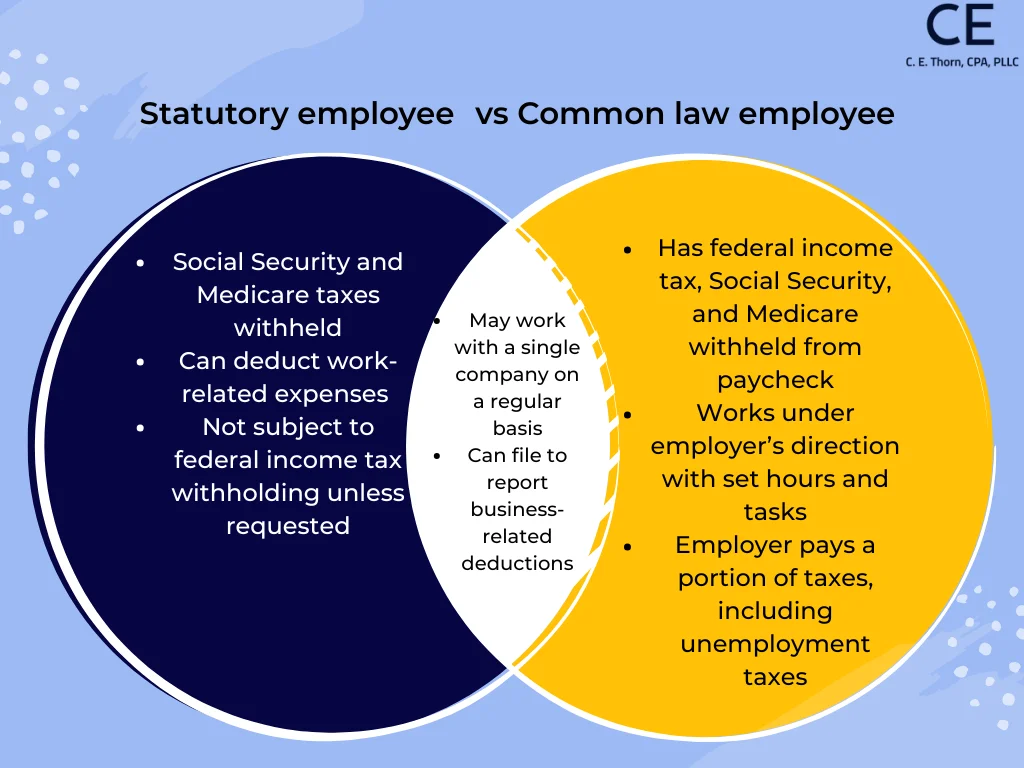

Statutory Employees vs Common Law Employees

Common law employees are traditional employees who work under the direction and control of the employer. These workers have federal income tax, Social Security, and Medicare withheld from each paycheck. Employers also pay a portion of these taxes, including unemployment taxes. Statutory employees, on the other hand, only have Social Security and Medicare withheld. Federal income tax is not automatically withheld, and they are not subject to FUTA.

Work Control and Benefits

Common law employees like retail cashiers, schoolteachers, or receptionists typically work at the direction of the employer—hours, tasks, and methods are all dictated by the company. In contrast, statutory employees have more flexibility and often use their own equipment, even if they work regularly with one company.

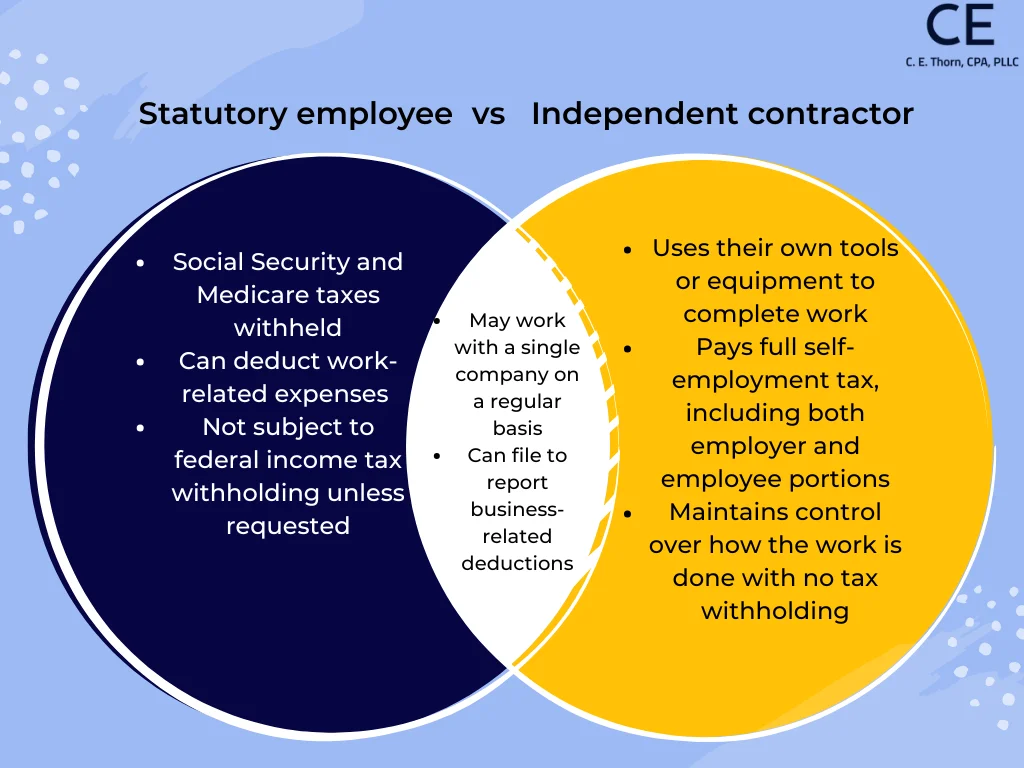

Statutory Employees vs Independent Contractors

Independent contractors are self-employed individuals who provide services to a business but maintain control over how the work is done. They pay the full amount of self-employment tax, including both the employer and employee portions of Social Security and Medicare. No taxes are withheld from their pay. Statutory employees, on the other hand, have Social Security and Medicare taxes withheld by the company, but can still deduct business expenses using a Schedule C, like independent contractors do.

Reporting Differences

Independent contractors, like freelance writers, web developers, and ride share drivers receive a 1099-NEC and file Schedule C and Schedule SE for taxes. Statutory employees receive a W-2 with a special checkbox marked and also file a Schedule C.

Statutory Employees vs Statutory Nonemployees

Statutory nonemployees are treated entirely as self-employed for tax purposes and belong to a limited category that includes direct sellers, licensed real estate agents, and certain companion sitters. These workers are treated as self-employed for all tax purposes. They receive no tax withholding and file a Schedule C like other sole proprietors. Statutory employees, by contrast, have Medicare and Social Security taxes withheld, creating a partial employer obligation.

Why Correct Classification Matters for Employers and Workers

Properly classifying workers is more than just an administrative formality—it has significant tax, legal, and financial consequences for both businesses and individuals.

Here’s why getting it right matters:

- Avoids IRS Penalties and Audits: Misclassifying workers (especially treating employees as contractors) can trigger audits and lead to back taxes, fines, and interest.

- Ensures Accurate Tax Withholding and Payments: Proper classification guarantees that the correct amount of Social Security, Medicare, and income taxes are paid—by the right party.

- Determines Access to Benefits: Employees may be entitled to unemployment benefits, workers' comp, and company-provided health insurance—while contractors and statutory employees typically are not.

- Clarifies Deduction Eligibility: Statutory employees and contractors can deduct certain business expenses, but traditional employees cannot under current tax law.

- Reduces Legal Liability: Misclassified workers may sue for unpaid benefits, overtime, or job protections if they believe they were incorrectly categorized.

- Promotes Trust and Transparency: Properly classifying workers builds a clearer, more professional working relationship and avoids confusion during tax season.

Contact Our Raleigh Small Business Accountants Today

Whether you're a business owner trying to correctly classify your workers or a contractor navigating complex tax forms, our team is here to help. At C.E. Thorn, CPA, PLLC, we provide reliable small business accounting services throughout Raleigh.

To learn more about our small business accounting services in the Raleigh area, call us today at 919-420-0092 or fill out the form below.